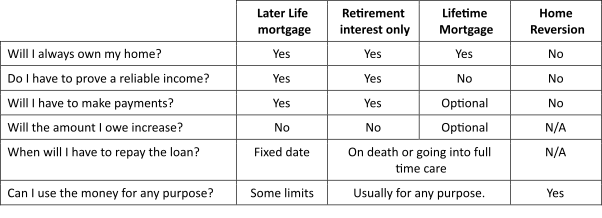

Retirement mortgage options

If you need to raise money and borrowing is the right way to do it, there might be alternatives to equity release.

Standard Mortgages for Later Life

Many lenders who offer standard mortgages have responded to the expectation that people will work well beyond the state retirement age. It is common to arrange a standard mortgage to age 75 and some lenders will consider applications up to age 90 or more. Most of the mortgage maybe available as interest only. A standard residential mortgage is likely to have a lower interest rate than an equity release option, which means that more of any payments you make will serve to pay off part of the loan.

However, you do have to show that you have enough income to meet the lender’s affordability requirements, usually from earnings. Also, the mortgage will have a fixed end date, so it is not a permanent option. A standard mortgage could be used to defer the time when an equity release option is needed.